Lease-end feels different in 2026. Whether you’re comparing new lease offers, shopping used cars, or buying out Mazda lease agreements, the next new car often comes with a higher sticker, a higher payment, and less room in the budget.

Inflation kept vehicle prices high. Interest rates are still elevated. Even used cars haven’t dropped enough to make starting over feel cheap.

That’s why more drivers are looking at vehicle value in a new way. Instead of handing back a car they already know, they’re weighing buyout options and smarter ownership moves.

Join The European Business Briefing

New subscribers this quarter are entered into a draw to win a Rolex Submariner. Join 40,000+ founders, investors and executives who read EBM every day.

SubscribeWhy leasing still makes sense, but only if you use it the right way

Leasing still fits a lot of people. Monthly payments are often lower than financing a new car, and you get a newer vehicle without planning for a long ownership run.

That matters in 2026, when higher prices and higher borrowing costs make every payment feel heavier. Leasing also works for drivers who want warranty coverage and don’t want surprise repair bills.

But the math has changed. Lease payments are up from pre-pandemic norms, and the old lease-and-repeat cycle doesn’t look as clean when each reset comes with a fatter bill.

Mileage limits matter more now, too. If your driving habits don’t match the contract, the lower monthly payment can turn into end-of-lease fees fast.

When a lease becomes a smart ownership opportunity

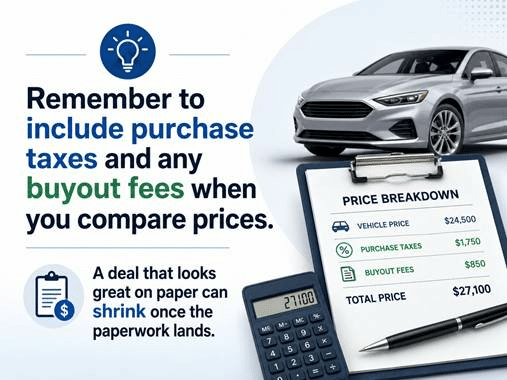

A lease buyout is simple. You pay the amount listed in your contract, plus the usual taxes and fees, and keep the car instead of returning it. A lease-end buyout isn’t sentimental. It’s a numbers decision.

If your buyout price is lower than what similar used cars sell for, you may already have value sitting in the driveway. Low mileage, clean history, and good condition can make that gap even better.

For drivers who like their car and plan to keep it, a lease can be a path to ownership instead of a dead end. You’re buying the vehicle you’ve already lived with, not gambling on a different used car with an unknown past.

So how do you know if your own lease belongs in that camp?

How to tell if your leased vehicle is worth keeping

This is where the decision gets real. A lease buyout is either a smart hold, or an expensive habit.

Check the buyout price against today’s market value

Start with the buyout quote from your leasing company. Then compare it with local asking prices for the same year, trim, mileage, and condition.

If the buyout is lower than the market, you may have instant equity. If it’s higher, you’re paying extra for the comfort of keeping a familiar car.

Don’t compare your car to the cheapest listing online. Match the details, or the math lies.

Look at mileage, condition, and repair history

Numbers matter, but so does the car itself. Low mileage, a clean maintenance file, no accident history, and light wear all make a buyout easier to defend.

One-owner history helps, too. So does a model with a solid reliability record and no pattern of costly repairs.

Heavy use changes the story. Body damage, bald tires, missed service, electrical issues, or an unreliable model can turn today’s buyout into next year’s repair bill.

A quick gut-check helps:

- Keep it if the car has been dependable, clean, and lightly driven.

- Walk away if you’re already bracing for repairs or the value feels soft.

- Pause and re-check the numbers if the buyout is close to market and the condition is only average.

Think about how long you’ll keep the car after the lease ends

Ownership works best when you’ll keep the car for a while. If you plan to drive it another five or six years, the buyout cost spreads out, and another round of lease payments stays off your back.

If you’ll want something else in a year or two, buying it may not pencil out. Short-term ownership can eat the savings once financing, taxes, and resale friction show up.

Ask one blunt question: are you buying this car, or are you buying time before the next payment? The answer usually clears things up fast.

Simple ways drivers are getting more value after the lease ends

Refinance, budget, and protect the car you already have

A buyout doesn’t end the cost conversation. Shop financing if the first rate looks rough. A credit union or local bank may beat the dealer’s offer.

Then set a maintenance budget and stick to it. Oil changes, tires, brakes, and routine service protect the car’s resale value and keep surprises smaller. That kind of routine care is boring, which is why it works.

Keep the car clean, inside and out. Fix small damage early. Neglect gets expensive twice, once in repairs and again when it’s time to sell.

Use off-lease value to avoid a pricier new car

This is where many drivers find the biggest win. Keeping an off-lease car can cost less than stepping into a brand-new one with a higher price, fresh fees, and pricier insurance.

You also dodge the churn. No new registration shock, no extra dealer add-ons, no starting over with a car you haven’t lived with yet.

Used car prices are still fairly high in 2026, even with more off-lease vehicles coming back into the market. That means a fair buyout can beat shopping from scratch.

Plan for resale before you sign the buyout

Think about resale before you buy the car. Keep every service record, stay on top of cosmetic issues, and don’t let mileage run wild if you know you’ll sell in a few years.

A well-kept vehicle is easier to trade and easier to sell privately. If you plan ahead, you’re not stuck guessing what it might be worth later.

Future value starts early. The choices you make right after the buyout shape what the car is worth when you’re ready to move on.

{kind=link}