Borrowing to buy or build your own space feels different in 2026. Owner-occupied commercial real-estate (CRE) quotes settled near 5.4 percent in late 2025 and—despite headline volatility—have stayed in the same tight band. A 10-year Treasury hovering around 4 percent keeps the bedrock cost of money predictable, while the Federal Reserve’s 3.50–3.75 percent target range has held for three straight meetings. With rate shocks off the table, the real question is which financing program fits your cash flow.

The menu is broader than ever—traditional banks, refreshed SBA 504 and 7(a) options, new SBA Green Lender pilots, fintech marketplaces, and quick (but pricey) bridge funds aimed at looming balloon dates.

Before we compare them, plug your wish-list numbers into Lendio’s free commercial mortgage calculator. Seeing the monthly payment in black and white will anchor the rest of this guide and keep every comparison grounded in your budget.

Join The European Business Briefing

New subscribers this quarter are entered into a draw to win a Rolex Submariner. Join 40,000+ founders, investors and executives who read EBM every day.

SubscribeOver the next few minutes we’ll rank seven credible funding paths, explain our scoring, and preview the rate landscape through 2026—so you can close the right loan, not just the first one offered.

How we selected and ranked your seven best options

We started with a long bench of more than 30 banks, credit unions, SBA programs, and fintech platforms that actively fund owner-occupied deals of five million dollars or less. Then we asked the same question you would: “Who gives a growing business the cleanest blend of price, leverage, and speed?”

To answer, we pulled fresh rate sheets, SBA debenture data, and February 2026 Fed releases. We calculated an apples-to-apples annual percentage rate (APR) for a typical purchase scenario: 75 percent loan-to-value, 25-year amortization, and standard closing costs. That APR became each candidate’s baseline score.

Cost alone never tells the whole story, so we layered in three tie-break factors: required equity, days to close, and credit leniency. A lender offering a low note rate but capping LTV at 65 percent fell below a slightly pricier rival willing to finance 90 percent. Programs that close in four weeks also earned bonus points over those that stretch past 90 days.

Finally, we double-checked every frontrunner against borrower reviews and regulatory data to confirm that the headline deals land on real closing statements. The result is a ranked short-list you can trust because it mirrors the way underwriters, not marketers, compare loans.

Next, you’ll meet the marketplace that tops the list and see how its single-application approach can arm you with multiple live quotes in one afternoon.

1. Lendio marketplace

Think of Lendio as the speed-dating host for commercial mortgages. You create one digital profile, upload tax returns, and the platform sends that package to more than seventy-five banks, credit unions, and fintech lenders.

Before you send a single document, Lendio’s commercial mortgage calculator lets you test loan sizes from $150,000 to $5 million and see exactly how APR and amortization shape the monthly payment, so you open negotiations with a number that already fits your budget.

Most business owners see their first term sheets within forty-eight hours. Typical offers land between 50 000 and five million dollars, reach up to 90 percent loan-to-value, and close in roughly four to eight weeks. Because every bid comes from an independent lender, the final rate can vary, but recent deal data shows low six percent notes for strong credits.

Why start here? Options. A single banker can only quote products on her shelf. Lendio sets a traditional five-year fixed from a regional bank beside a 25-year SBA 504 structure and a flexible seven-year hybrid from a credit union. You see the trade-offs—rate, fees, and speed—side by side before chasing paperwork.

The marketplace model also reveals niche programs local borrowers rarely hear about, such as community-development credit unions that finance mixed-use storefronts or fintech partners piloting rapid-close green-retrofit loans. If your cash flow feels tight or your property is unconventional, those fringe bids can mean the difference between “declined” and “cleared to close.”

One caution: Lendio is a broker, so you still negotiate final terms with the lender you choose, and some banks add their own diligence fees. Read each term sheet as if it were the only one on your desk. Starting with a broad view usually sharpens your negotiating edge and is worth the 15-minute application.

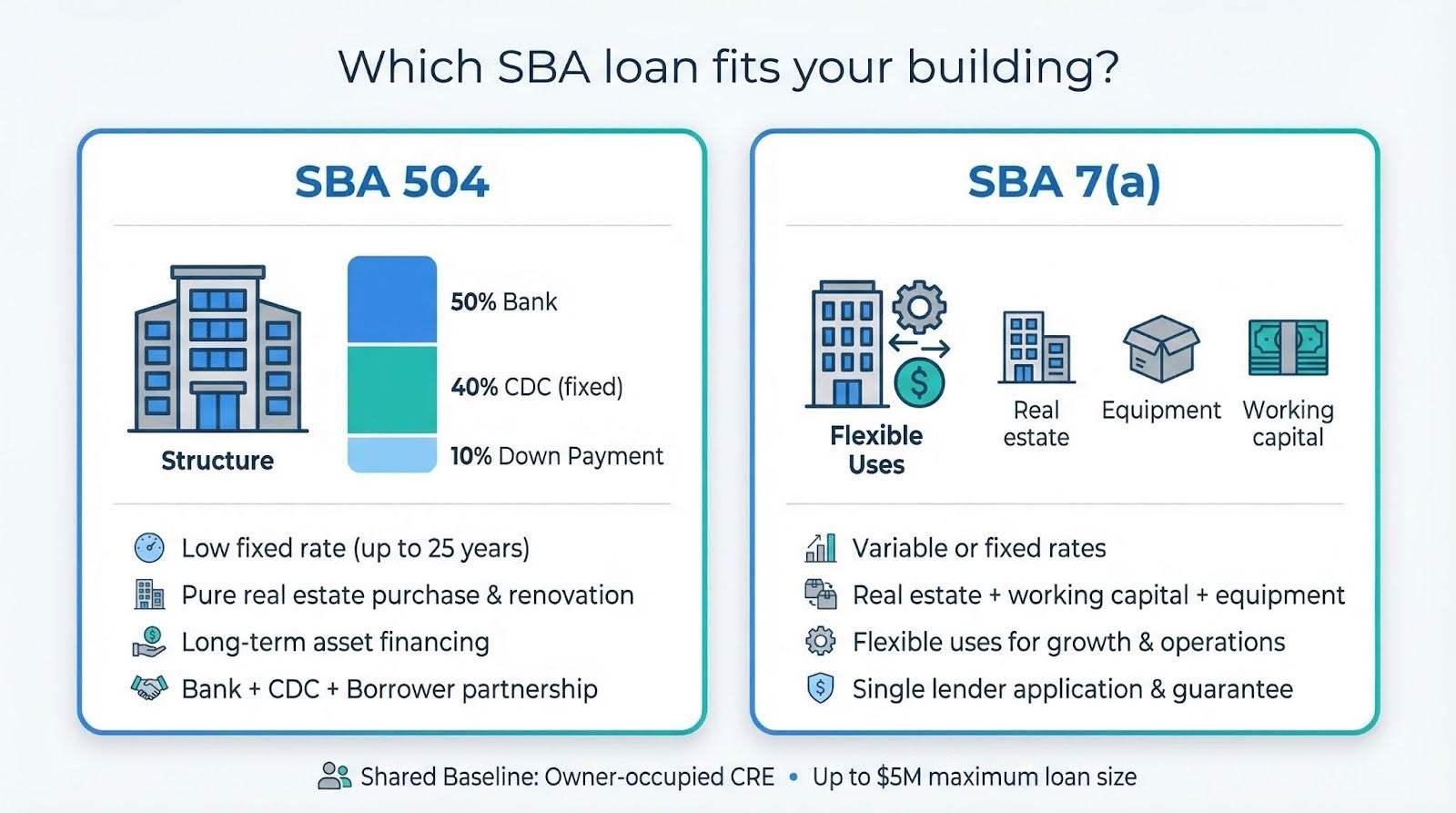

2. SBA 504: long-term, low-rate heavyweight

If you plan to own your building for decades, the SBA 504 program can feel like a trusted ally in a blazer and flats.

Here is the structure in plain English. A bank funds 50 percent of the purchase, a Certified Development Company (CDC) covers 40 percent, and you supply the final 10 percent as equity. Because the CDC piece is backed by a government-guaranteed debenture, its rate stays eye-catchingly low, about 5.7 percent fixed for 25 years as of March 2026. Blend that with a market-rate senior note and you have one of the cheapest long-term payments available.

The math gets even kinder when you look closer. Financing 90 percent of a $2 000 000 warehouse preserves $200 000 in cash compared with a bank that caps leverage at 75 percent. Stretching repayment over 25 years instead of 20 cuts the monthly payment by roughly 12 percent, money you can redirect toward equipment or payroll.

Great terms do not arrive overnight. Plan on 60 to 90 days from letter of intent to funding. You will sign a personal guarantee and must occupy at least 51 percent of the space. On the plus side, manufacturers benefit from partial fee waivers, and many CDCs host virtual workshops to speed the paperwork.

Bottom line: If your business will stay put and you want the predictability of a fixed rate below six percent, the 504 deserves a spot at the top of your shortlist.

3. SBA 7(a): the Swiss-army knife of business financing

Sometimes you need one loan that wears more than one hat. The SBA 7(a) program fits those moments when buying a building, refinancing equipment debt, and stocking inventory all collide in the same quarter.

Here is the draw: one request of up to five million dollars can finance real estate at up to 90 percent loan-to-value, roll in working capital, and stretch repayment to 25 years on the property portion. Rates float off the Prime index, currently 8.50 percent, plus as little as one point for strong borrowers. Fixed-rate options exist too and have been settling in the mid-six percent range for seasoned, low-risk credits.

Flexibility extends beyond use of funds. Start-ups with a solid business plan, borrowers lacking collateral, and companies rebounding from a tough year often clear 7(a) underwriting when banks say no. Preferred Lending Partners send files straight to the SBA e-Tran system, trimming weeks off approval compared with the traditional channel.

Trade-offs remain. Variable pricing means your payment can rise if the Fed lifts Prime. Closing costs sit higher than conventional loans because you pay a government guarantee fee. Underwriting also digs deep with full financial statements, global cash-flow analysis, and personal guarantees for anyone owning 20 percent or more.

Still, if you prize adaptability and want one loan that grows with the business, the 7(a) delivers. It is the pocketknife that folds out the exact tool you need when the project list gets messy.

4. Relationship banks and aggressive credit unions

Sometimes the lowest rate lives where your checking account already sits. Large relationship banks such as Wells Fargo, U.S. Bank, and many hometown community lenders still dominate owner-occupied mortgages. Their access to low-cost deposits lets them quote headline rates starting near 5.75 percent for pristine borrowers. Pair that with a 20-year amortization, and the payment often feels almost residential.

Credit unions can go even lower. Because they answer to members, not shareholders, many advertise promos between five and six percent to capture medical offices and professional-services condos. They are selective, though. Plan on a maximum 80 percent loan-to-value, a personal guarantee, and at least two consecutive profitable years.

Speed is the quiet perk. An existing deposit customer with organized books can move from application to clear-to-close in about 30 days. Underwriters pull statements straight from internal systems, so you avoid much of the paperwork a new-to-bank borrower must supply.

Still, the gatekeepers have standards. Banks like to see a global debt service coverage ratio above 1.25 and credit scores over 700. They also prefer that you contribute 25 to 35 percent cash, a hurdle for fast-growing firms that reinvest every dollar.

Use this knowledge to your advantage. If your numbers shine, walk into the branch and ask for the private-client CRE grid. Get the quote in writing, then invite marketplace lenders or an SBA 504 partner to top it. At worst, you confirm you already hold the cheapest money in town; at best, you persuade the banker to trim another quarter point to keep your accounts.

5. Nonbank and fintech lenders: speed with a price tag

Picture a lender that thinks more like a software start-up than a bank branch. That is the feel at RCN Capital, Breakout Capital, and several similar funds now courting small CRE deals under three million dollars.

Their pitch is simple. Upload bank statements, a rent roll, and a recent appraisal. Within a week you can have a term sheet that ignores the rigid debt-service ratios legacy banks recite. Many will approve 75 percent loan-to-value on an owner-occupied warehouse even if last year’s tax return looks choppy.

Turn time is the headline perk. Closings often land inside 30 days because these lenders keep underwriting, legal, and servicing in-house. That agility lets you lock a site before a competitor or refinance a balloon note without losing sleep.

The cost shows up in the rate column. Most funds price 200 to 300 basis points above bank offers, so expect interest in the upper six to mid-eight percent range for well-qualified borrowers. Origination fees run one to three points, and many loans reset or balloon after seven to ten years.

Who wins here? Entrepreneurs with strong growth stories but thin collateral, contractors running projects through multiple entities, and buyers in secondary markets ignored by big-city banks. If time is your enemy or traditional credit metrics paint an unfair picture, a fintech lender can be the fast lane; just confirm the extra interest still pencils out over the hold period.

6. Hard-money and bridge loans: when the clock is louder than the rate

Every so often the calendar, not the calculator, drives the deal. A seller gives you 14 days to close. A maturing note needs a payoff by month-end. That is when hard-money bridge lenders step in.

These funds prize collateral and exit strategy above all else. Provide a solid appraisal, a clear title, and proof you can refinance or sell within 12 months, and they can wire cash quickly, often in two to three weeks. Loan-to-value caps at about 75 percent, payments are interest-only, and paperwork is slimmer than a standard bank term sheet.

Speed carries a premium. Current bridge quotes cluster between 9 and 12 percent, with one to three points due at closing. The rate stings, yet it buys valuable breathing room. Investors use the bridge to renovate, stabilize rent rolls, or cure credit blemishes before moving back into conventional financing.

Hard-money is temporary, so schedule the refinance plan on day one. Lenders will ask for it, and your wallet will thank you when the high-cost debt rolls off the books.

If you need certainty tomorrow morning more than the lowest payment over 20 years, bridge funding is the emergency lever. Pull it with intent, finish the turnaround, then return to calmer waters.

Interest-rate backdrop and the road to 2027

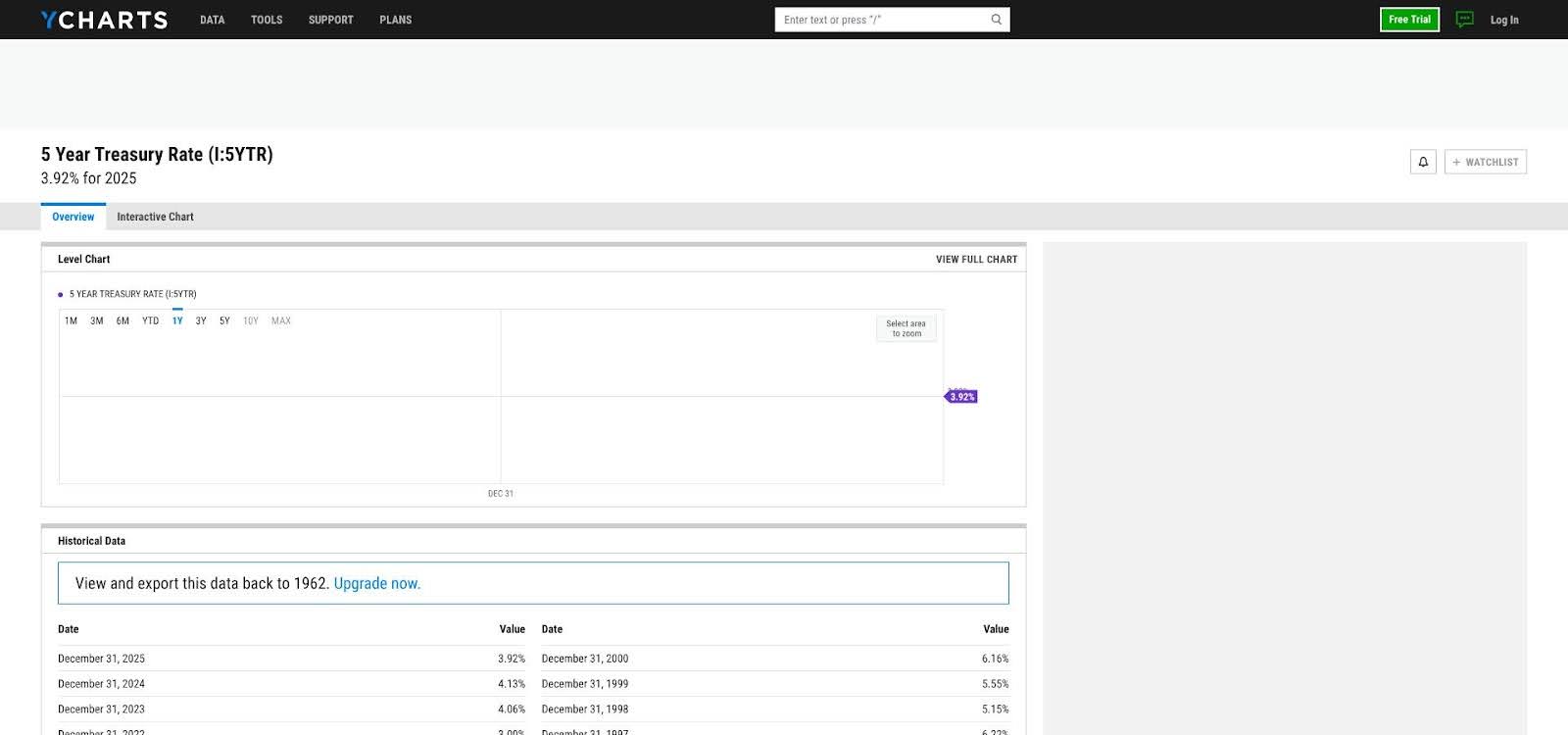

Rates feel calm today, but the tape tells a rough story. Five-year Treasuries bottomed near 0.9 percent in early 2021, then climbed to 3.7 percent by March 2026, quadrupling in five years, according to YCharts Treasury data.

5-year Treasury rate trend 2021–2026 for commercial loan context

According to Growth Corp, the 25-year SBA 504 fix sat in the low threes before COVID, peaked above six in 2025, and eased to 5.86 percent this February.

Terry Dale Capital’s February 2026 market update suggests bond traders expect two quarter-point Fed cuts by late 2026, yet incoming Chair Kevin Warsh says he will “keep policy restrictive until core inflation sits sustainably near target.” Markets translate that stance into slower, smaller relief.

What does that mean for you?

- Fixed-rate loans tied to Treasuries may drift sideways, which helps you lock long-term debt while yields remain below last year’s highs.

- Variable-rate 7(a) notes move with Prime, so every Fed decision appears in next month’s billing notice.

- Bridge and hard-money lenders watch credit spreads, not the Fed; if recession talk rises, expect their coupons to edge higher even as benchmarks fall.

Smart next steps: match the loan term to your exit horizon, pad pro-formas for one extra rate hike, and set a reminder six months before any reset date. A little foresight now prevents a scramble later.

FAQs: commercial loan cheat-sheet

How do I snag the lowest rate?

Start with the basics — credit score above 700, debt-service coverage north of 1.25, and at least 10 percent cash in the deal. Then shop hard. Use the Lendio marketplace for a broad view, pull a quote from your relationship bank, and test an SBA 504. Present competing term sheets to every lender; nothing trims a margin faster than a credible alternative.

What loan-to-value will banks accept right now?

Most conventional banks land between 65 and 75 percent. Credit unions can reach 80 percent for pristine files. If you need 90 percent, pivot to SBA territory; both 504 and 7(a) can go that high when you occupy the building.

Should I lock a fixed rate or float with Prime?

Match the term to your horizon. Holding the property long term? Take the sure thing and fix it. Planning to refinance or sell within five years? A variable 7(a) saves upfront interest and lets you benefit from any Fed cuts; just budget an extra 50-basis-point safety buffer.

What is the real difference between SBA 504 and 7(a)?

Think of 504 as a pure real-estate mortgage: low fixed rate, long amortization, and strict occupancy. A 7(a) loan works like a flexible credit line wrapped in a mortgage; it handles mixed uses such as buying a building and funding inventory. Fees run higher on 7(a), but you trade cost for versatility.

Can I refinance a hard-money bridge into an SBA loan?

Yes, if the property is owner-occupied and your business meets SBA size standards. Start the SBA application the day your bridge funds, because you will need fresh appraisals and environmental reports before that 12 percent note matures.

Keep these answers handy. They will save you a late-night forum scroll when the lender’s email pings your inbox.

Putting it all together

Commercial real estate financing in 2026 boils down to three decisions:

Choose your leverage. Decide how much cash you want to keep working in the business versus tying up in the building.

Choose your speed. Balance the comfort of a 90-day SBA closing against the rush of a two-week bridge.

Choose your rate risk. Fix for the long haul if you are building generational wealth, or float with Prime when a refinance sits on the calendar.

Every lender we covered solves a different blend of those trade-offs. Stack their term sheets on your desk, run the payments through the commercial mortgage calculator, and pick the one that lets you sleep at night and grow in the morning.

We wish you low rates, smooth appraisals, and a closing table full of celebratory coffee cups.

{kind=link}