EBM WEEKEND READ: By Nick Staunton

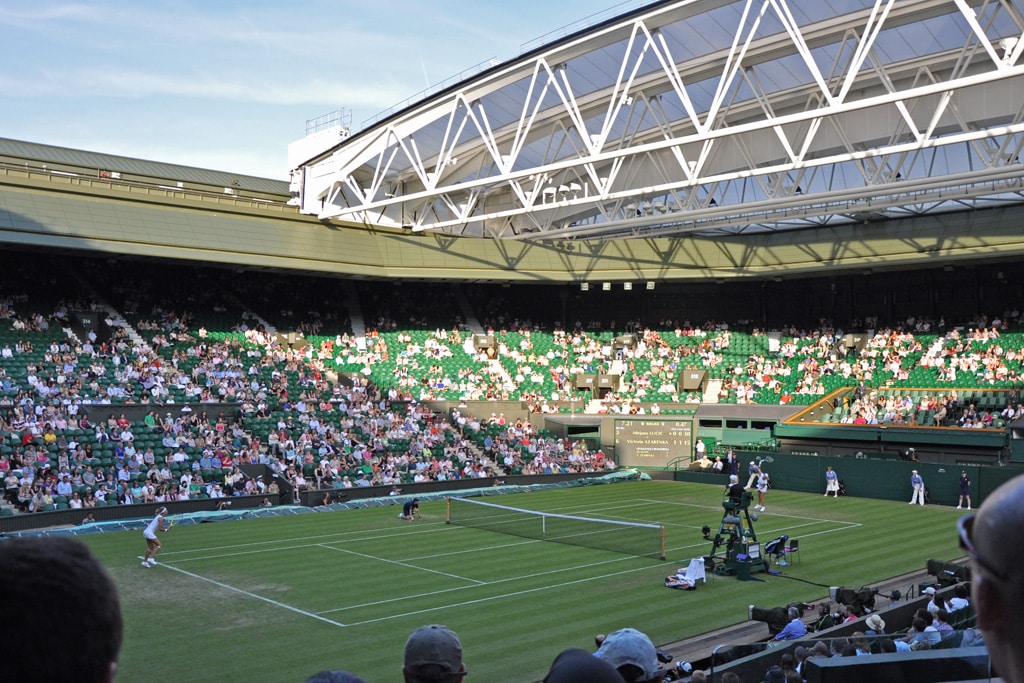

Updated:London -Saturday 4rth of July-Every July, roughly 500,000 people descend on a corner of south-west London to watch tennis, eat strawberries, and queue for hours in the hope of getting a ticket. This year’s Championships got underway on 29 June and are now into the third round. The tournament they are queuing for generates close to £400 million in revenue across fourteen days of play. It pays out £64.2 million in prize money this year, a 20% increase on 2025. It is broadcast in 220 countries. The US broadcasting deal alone — ESPN signed a twelve-year contract worth a reported $95 million per year — is worth more annually than the entire transfer budget of many Premier League clubs.

And yet there is no logo on the court. No title sponsor. No shirt deal. No outside investors. No private equity. No sovereign wealth fund. The whole thing is run by a private members club with fewer than 500 members — the same restraint that has helped turn past champions like Roger Federer’s tennis fortune into one of sport’s cleanest commercial case studies, even as others who won here, like Boris Becker’s $50m collapse, show a title alone guarantees nothing.

This is Wimbledon, mid-Championships in 2026. And the business model behind it is unlike anything else in professional sport.

Join The European Business Briefing

New subscribers this quarter are entered into a draw to win a Rolex Submariner. Join 40,000+ founders, investors and executives who read EBM every day.

SubscribeWhat Wimbledon Actually Earns

Start with the money. Wimbledon reported total operating revenue of approximately £380 to £400 million in 2025. Nearly half of that — close to £200 million — came from global broadcast rights.

The BBC has broadcast Wimbledon for 88 years. The current deal, which runs until 2027, is worth £44 million per year. ESPN’s deal, running from 2024 to 2035, is worth $95 million per year — the single largest media contract in the tournament’s history. These are not deals struck by a desperate rights holder taking whatever it could get. They are deals negotiated from a position of complete control, because Wimbledon owns its broadcast rights outright. It does not sell them to a league body, which then distributes them across clubs. It keeps them, packages them, and licences them directly to broadcasters around the world.

That is the first and most important thing to understand about Wimbledon’s business model. Control. Total, institutional, unapologetic control over every commercial decision the tournament makes.

Sponsorship: Fewer Partners, Higher Prices

Sponsorship contributes another significant slice. Wimbledon had 17 sponsors in 2025, generating a combined annual value of around $124 million. Barclays — the tournament’s official banking partner since 2023 — pays approximately £20 million a year. Emirates, the official airline, pays $12 million. Rolex, Robinson’s, Evian, IBM. Every partner is chosen carefully, paid well, and kept off the courts. No courtside advertising boards. No sponsor logos on the playing surfaces. The All England Club believes — and 148 years of evidence supports the belief — that the scarcity and cleanliness of Wimbledon’s visual identity is itself a commercial asset worth more than the revenue it forgoes by refusing mass sponsorship.

The Australian Open has 40 sponsors. Roland Garros and the US Open each have around 30. Wimbledon has 17, earns less from sponsorship as a result, and commands a higher price per partner because of it. Scarcity creates premium. Premium creates desirability. Desirability creates scarcity. The loop sustains itself — the same logic that has made a Wimbledon championship one of the most commercially valuable titles an individual player can hold, regardless of what happens to that value afterward. It is also why the players who convert a Wimbledon title into lasting commercial weight, rather than simply banking the prize money, tend to be the ones who go on to build tennis’s biggest fortunes well beyond their playing careers.

The Debenture System — Genius Hidden in Plain Sight

Here is the part of the Wimbledon business model that almost nobody outside the financial world fully appreciates. The debenture system.

A Wimbledon debenture is a financial instrument — regulated by the Financial Conduct Authority — that gives the holder a guaranteed prime seat on Centre Court or No.1 Court for every day of the Championships over a five-year period. They are issued in blocks, cover five consecutive tournaments, and are freely transferable. You can sell your seat on the days you cannot attend. You can sell the debenture itself on the secondary market.

The latest Centre Court debentures — covering 2026 to 2030 — were priced at £116,000 each. The All England Club issued 2,520 of them. If all sold, that is approximately £292 million raised in a single issuance, without a bank loan, without diluting ownership, without taking on a single outside investor. No interest payments. No lenders to satisfy. Just capital raised directly from people who want guaranteed access to the most coveted tickets in sport.

No.1 Court debentures for 2027 to 2031 are priced at £73,000 each — up 60% from the previous cycle’s £46,000. The 1,250 debentures on offer could raise over £90 million.

Think about what this means in practice. Wimbledon is essentially raising hundreds of millions of pounds in interest-free financing from its most passionate supporters, who are simultaneously grateful for the privilege. The fans are the lenders. The tournament is the borrower. And the borrower never pays interest.

The contrast with how European football clubs finance their ambitions could not be more stark. Football clubs took on debt from private equity firms, gave away equity, and now face exit pressure from investors who need their returns. Wimbledon raised the equivalent amount from fans who consider the arrangement a privilege and will queue to do it again when the next cycle opens.

The SW19 Land Bank

Wimbledon does not just own a tennis club. It owns land in one of London’s most valuable postcodes.

Wimbledon does not just own a tennis club. It owns land in one of London’s most valuable postcodes.

The All England Club purchased the neighbouring Wimbledon Park Golf Club for £65 million — buying out the lease that had restricted its use of the 73-acre site. That land, in SW19, is now being developed into a third show court, additional practice facilities, and expanded infrastructure. The capital value of the All England Club’s landholding in south-west London — including the existing site and the golf club land — runs well into hundreds of millions of pounds at current market values.

This is permanent, appreciating capital. It does not appear on a quarterly return target. It does not need to be liquidated in five years to satisfy a fund’s investors. It just sits there, increasing in value, securing the institution’s independence.

The Strawberries and the Margin

The hospitality operation at Wimbledon is a masterclass in high-margin experience pricing.

Around 500,000 people attend across the two weeks. Catering, merchandise, and hospitality contribute meaningfully to the overall revenue figure. Wimbledon sells approximately 150,000 portions of strawberries and cream during the tournament — at £3.50 per serving in 2025, unchanged for years as a deliberate pricing and brand decision. The restraint on that one item is itself a marketing move. It says: we are not here to extract maximum revenue from every transaction. We are here to maintain an experience.

Meanwhile the hospitality packages — private suites, corporate entertaining, debenture holder restaurants — operate at the opposite end of the pricing spectrum. This is where the real margin sits. A corporate hospitality package at Wimbledon costs thousands of pounds per person per day. The demand consistently outstrips supply. The same logic that drives premium pricing across luxury goods and financial services applies here: scarcity is the product, and the price reflects it.

Why Nobody Can Copy It

The Wimbledon model is frequently admired and never successfully replicated. The reason is simple. It took 148 years to build.

The debenture system works because people believe Wimbledon will exist in twenty years and be worth attending. That belief is earned over generations, not manufactured by a marketing campaign. The broadcast premium works because Wimbledon is genuinely the most prestigious tennis tournament on earth — a status built on grass courts, royal patronage, and a refusal to compromise on aesthetics for a century and a half. The land bank works because the All England Club bought its site before London SW19 became one of the most valuable squares of real estate in Europe.

You cannot create this from scratch. The private equity firms now trying to exit their football investments understand this better than anyone — they arrived with capital and commercial expertise, and found that the thing they most wanted to monetise, the emotional connection between a club and its supporters, was precisely the thing that resisted monetisation most stubbornly.

Wimbledon never tried to monetise that connection. It simply maintained it. And the connection kept generating revenue on its own.

The Surplus Goes to British Tennis

There is one final element of the Wimbledon model that deserves attention.

When revenue exceeds costs — when the tournament generates a surplus — 90% of it goes to the Lawn Tennis Association to invest in British tennis. The institution exists not to maximise its own profit but to sustain the sport it represents. It takes no outside capital. It pays no dividends to investors. It distributes its surplus back into the game.

Revolut targets a $200 billion IPO valuation. SoftBank is borrowing $40 billion to bet on OpenAI. Private equity is trying to figure out how to exit football clubs it bought at peak valuations. And in a corner of south-west London, a private members club with fewer than 500 members is quietly generating £400 million in revenue across two weeks every summer, with no debt, no outside shareholders, and no logo on the court.

The most sophisticated sports business model in the world does not look like a business at all.

That is precisely why it works.

Related Analysis

{kind=link}