EBM Weekend Read | London, 3 May 2026

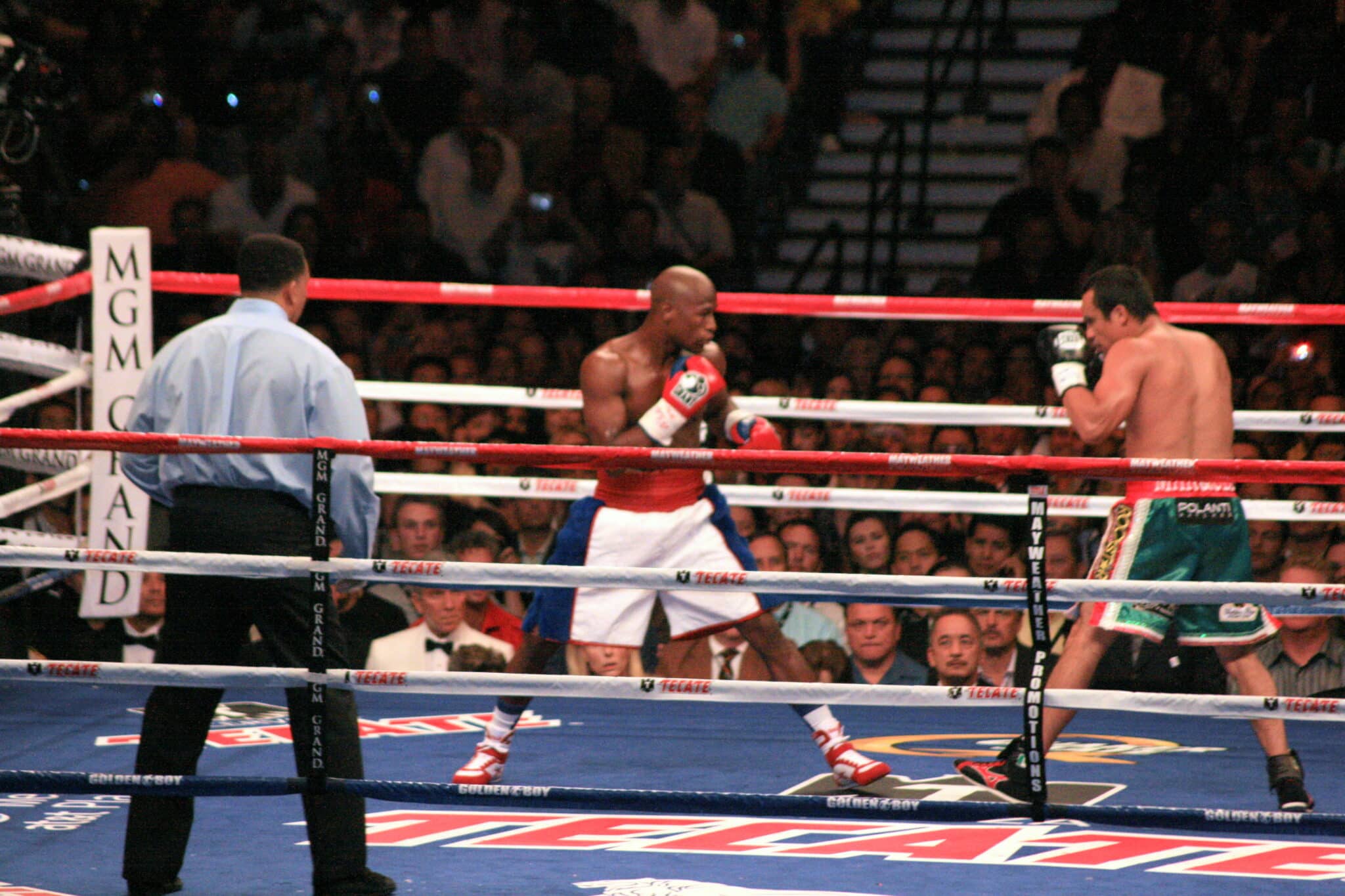

On 2 May 2015, Floyd Mayweather Jr. defeated Manny Pacquiao at the MGM Grand in Las Vegas. The fight generated approximately $600 million in revenue across pay-per-view, gate receipts and closed-circuit broadcast — the most lucrative single sporting event in modern history. Mayweather’s share, per ESPN’s reporting at the time, settled between $220 and $230 million.

Pacquiao, the loser on the scorecards, took home roughly $150 million on the agreed 60-40 split. But that figure did not last long inside Pacquiao’s bank account. The Filipino had to pay his promoter, Bob Arum’s Top Rank, a contractual cut of his purse — a fee that, according to industry reporting, ran into double-digit millions. Mayweather paid no such fee. He owned his own promotion. The same difference, repeated across fourteen pay-per-view events generating $1.3 billion of cumulative revenue, is the most important commercial story in modern boxing.

It is also one of the cleanest case studies in vertical integration any sport has produced. Long before Saudi Arabia spent $6 billion trying to build LIV Golf, and long before private equity began circling Europe’s most valuable football clubs, Mayweather had already worked out the principle that defines modern athlete economics. The fighter is the asset. The fighter should own the asset.

Join The European Business Briefing

New subscribers this quarter are entered into a draw to win a Rolex Submariner. Join 40,000+ founders, investors and executives who read EBM every day.

SubscribeThe structure every other fighter accepted

For most of boxing’s commercial history, the economic structure of the sport ran in one direction. Promoters owned the events. Networks owned the broadcast rights. Sanctioning bodies owned the titles. Fighters owned their fists.

Don King and Bob Arum, the two most powerful promoters of the late twentieth century, built fortunes on a model that was not, on paper, exploitative. The promoter took on the financial risk of staging the event, fronted marketing costs, and negotiated with networks and casinos. In return, the promoter took a contractual percentage of the fighter’s purse — typically 25 to 33 per cent of net earnings on a major bout, sometimes more on smaller cards.

The arithmetic was unambiguous over a career. A fighter generating $50 million in lifetime purses might pay a promoter $12 to $15 million across that career. For a top earner like Mike Tyson, generating $400 million in career purses, the promoter cuts ran into the high tens of millions — money that left the fighter’s column and arrived in the promoter’s column for work that, in many cases, the fighter could plausibly have done himself with the right team.

Tyson was not unusual. Sugar Ray Leonard, Lennox Lewis, Oscar De La Hoya, Roy Jones Jr — all of them ran their careers within the promoter system. Some of them made attempts to break it. De La Hoya founded Golden Boy Promotions in 2002 and successfully promoted his own later fights. Lewis became a partner in Lion Promotions. But none built a vertically integrated structure that meaningfully shifted the lifetime economics in the fighter’s favour. The system absorbed them.

What Mayweather did differently

Mayweather Promotions was incorporated in Las Vegas in 2007. The trigger was the De La Hoya fight that same year — a bout that generated $136 million in pay-per-view revenue, made Mayweather $25 million on a then-typical purse split, and demonstrated unambiguously that Mayweather’s name on a card moved the commercial needle independent of any promoter’s brand.

The structure Mayweather built was deliberately simple. Mayweather Promotions secured network output deals directly with HBO and later with Showtime, bypassing intermediary promoters entirely. The company contracted Mayweather’s own fights, retained the promotional fee that would otherwise have gone to Top Rank or Golden Boy, and kept full control of marketing, branding, and ancillary revenue streams — merchandise, sponsorship inventory at the venue, broadcast credit positioning.

The economic difference compounded with every fight. On the De La Hoya bout in 2007, Mayweather paid an external promotional fee. By the Pacquiao fight in 2015, every cent of the promotional revenue stream was internal. ESPN’s coverage at the time spelled it out plainly. Pacquiao’s net take from the $150 million purse “will be significantly reduced after paying off his promoter, Bob Arum and Top Rank.” Mayweather had no such deduction. The result was a $30-to-50 million swing in Mayweather’s favour from a single fight, before any consideration of differential talent, marketing, or networking.

Across his fourteen pay-per-view bouts, this structural advantage compounded into something approaching half a billion dollars in retained earnings that, under any traditional promotional model, would have left the fighter’s column.

The CompUSA-vs-Apple-Store insight

The strategic principle Mayweather grasped earlier than the rest of his sport is the same one Apple grasped against the consumer-electronics retail model in the early 2000s. When you control distribution, the margin in distribution is yours to keep. When you outsource distribution, the margin in distribution is your distributor’s to keep. Apple opened its own stores and absorbed the retailer margin. Mayweather opened his own promotion and absorbed the promoter margin.

The principle scales beyond either example. It is what music artists are now doing when they leave major labels to build owner-operated distribution through Spotify and Apple Music direct-deal arrangements. It is what Hollywood stars are doing when they form production companies that retain back-end participation rather than accepting flat fees. It is what European sports teams are doing when they build direct-to-consumer streaming products rather than selling all rights to broadcasters.

In every case, the underlying logic is the same: the high-value individual or asset accepts the higher operational complexity of running their own distribution in exchange for the structural margin that the distribution layer would otherwise extract.

The discipline that made it work

Mayweather Promotions was not a vanity project. It was operationally serious from the beginning. Leonard Ellerbe, Mayweather’s CEO and a long-standing business partner, ran the company on the same disciplines as any well-managed media business. Costs were controlled. Network deals were renegotiated annually with leverage that grew with every fight. Younger fighters were signed to the promotion — Adrien Broner, Badou Jack, Gervonta Davis — extending the company’s revenue base beyond Mayweather’s own diminishing fight calendar.

By the time Mayweather retired from active competition in 2017, Mayweather Promotions had a stable of contracted fighters, a continuing network deal pipeline, and a brand that travelled internationally. The post-retirement exhibition bouts — McGregor in 2017, Logan Paul in 2021, sundry low-impact spectacle fights since — all ran through Mayweather Promotions. Mayweather kept the promotional margin on his own retirement.

For European business readers watching parallel disruptions in football, motorsport and luxury sport sectors, the Mayweather lesson scales directly. The economic surplus in any high-value entertainment industry tends to flow toward whoever controls the distribution and rights layer. Athletes, performers, and creators who accept the traditional structure — agent, manager, label, promoter, broadcaster — leave structural margin on the table. The ones who build vertically integrated personal businesses keep it.

The ledger, twenty years on

Mayweather is widely reported to have earned over $1 billion in his boxing career. That figure undersells the strategic point. Tyson earned approximately $400 million in his career and ended up bankrupt. Pacquiao earned approximately $575 million across his career, paid extensive promoter fees throughout, and has had well-documented financial difficulties. Holyfield, De La Hoya, Roy Jones Jr — all earned hundreds of millions, all had complex post-career financial situations. Mayweather, by every account, retired solvent, diversified, and operating across real estate, private equity, and media businesses through entities he owns directly.

The difference is not lifetime earnings. It is retained equity. Tyson’s $400 million flowed through promoter accounts, network accounts, manager accounts, accountant accounts. Mayweather’s $1.3 billion in PPV revenue flowed substantially through one accounting structure: his own.

That, in the end, is the case study. Boxing was not the asset. The asset was Floyd Mayweather. Mayweather was the only fighter of his generation who treated himself accordingly. Every other fighter before him left money on the table — money the promoters received instead. The structure Mayweather built was not innovative on the talent side. It was unprecedented on the ownership side. The lesson, decades on, is one any athlete, performer, or owner-operator entering a high-margin distribution industry should study at length.

Related Analysis

Elon Musk Will Soon Be Worth More Than Saudi Arabia’s Sovereign Wealth Fund

Why Saudi Arabia Just Walked Away From a $6 Billion Golf Bet

Real Madrid Hit €1 Billion — Europe’s Richest Football Clubs Ranked by Revenue

{kind=link}